![]()

Passive vs. Active

Submitted by Kaizen Financial Advisors, LLC on March 17th, 2017

There are numerous ways in which investment funds are classified. One that has been the topic of much debate over the years is passive vs. active. The difference between the two is simple. Active funds manage a portfolio of securities using strategies that attempt to time the market, utilize research to identify superior performing securities, and implement market driven strategies to determine what to buy and sell. Active funds pay large sums to fund management, research, and fund operations. Passive funds are just the opposite. Their only strategy is to match a known index, for example, the S&P 500. Passive funds do not need expensive managers, or research teams, they tend to make few trades, and operational expenses are low.

On average, active funds tend to be more expensive to own for the reasons stated. It’s not uncommon to find active fund expense ratios that are 2 to 10 times larger than comparable passive funds. Their larger expense burdens would be gladly be paid by shareholders, if performance compensated the expense differential. This performance vs cost comparison is at the crux of the active/passive debate.

The research company Morningstar is a leading provider of research related to investment funds. Every quarter, Morningstar publishes the “Active/Passive Barometer” to shed light on this debate. I will share some of the finding published in the 2016 year-end edition.

I would like to introduce the metric “Active fund success rate”. As the name implies, it depicts the percent of active funds that outperform their passive counter parts over various time frames. Funds are only measured against funds of comparable asset classes. For example, domestic large cap value funds are only compared against other domestic large cap value funds. Both the active funds and passive fund performance is measured after fees.

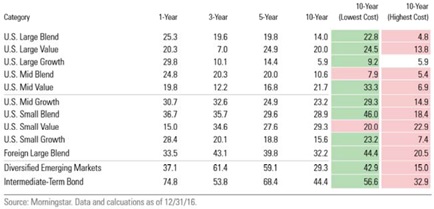

Some active funds are more expensive than others. Is expense synonymous with quality? Stated another way, does spending more on fund managers and research produce better performance? Let’s take a look. First we stratify active funds by their expense ratio and then compare performance across the 12 major Morningstar asset classes. Study the chart for a few minutes.

Active fund success rate by asset class

From the table above, we see that lower cost funds over the past 10 years out perform high cost funds in nearly every asset class category. The numbers show what percentage of active funds have outperformed their passive counterparts (if the percent is greater than 50%, then active outperformed passive, if less than 50%, then passive outperformed active). Here is the other big take away. Over the past 10 years, only low-cost active intermediate-term bond funds out performed its passive counterpart, and it wasn’t by much (the active success rate was only 56.6%). In fact, the longer the time horizon the greater the likelihood that passive will outperform active.

There is another factor to consider that favors passive funds. The data above requires the fund to survive for at least 10 years. When performance suffers for a prolonged time period, active funds will often shut down and move current shareholder into a better performance active fund in the same space. For example, if we focus in on US Large Cap stock funds, we find that roughly half the funds from 10 years ago were shut down before their 10th anniversary. Had they all survived, I can only speculate the percentage that outperformed passive would be even smaller than the data depicts.

So here are the key takeaways we should glean from this data

-

There have been individual years (short timeframes) where active funds have outperformed passive funds

-

On average, actively managed funds underperform their benchmarks over longer time frames.

-

The longer the time horizon, the lower the percent of active success, and the greater the passive advantage appears to be

-

Lastly, performance is inversely proportional to expenses, that is, high expenses translates to worse performance

If this information is readily available, then why do people invest in active funds? In short, marketing. Psychologically, people like believing that having someone at the wheel will improve performance, after all, these are smart people right? When these funds do outperform, they advertise heavily. Unfortunately these added costs generally has not translated to the performance they had hoped for.

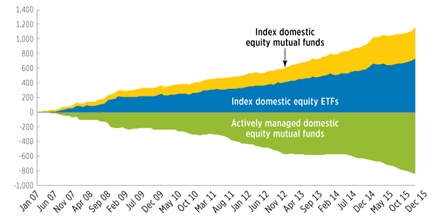

That said, there are signs that investors are catching on. Over the past 10 years, net cash flows OUT of actively managed mutual funds was nearly a trillion dollars. Over that same time, more than trillion dollars flowed INTO passively managed mutual funds and exchange traded funds. There is an old adage, “follow the money”. This a trend I believe will continue and the prevailing data, whether from Morningstar or from the academic community, explains why.

Cumulative Flows to and from Active and Passive Funds

Sources: Morningstar’s “Active/Passive Barometer”, Year-end 2016;

Investment Company Institute, “2016 Investment Company Fact Book”

This material is subject to the copyright protection of Kaizen Financial Advisors, LLC and its agents and employees (collectively, “Kaizen”) and may not be reproduced in part or in whole without the prior written consent of Kaizen. This material is not intended for distribution to, or to be used by, any person or entity other than the person or entity to whom this was originally delivered. This material is also not intended for distribution in any jurisdiction in which distribution would be contrary to law or regulation.

Furthermore, this material is for general educational and informational purposes only. Although the information was compiled from sources believed to be reliable, Kaizen does not assume any responsibility for its accuracy or completeness. This material is not meant to replace independent professional judgment and should not be relied upon as legal, financial, tax or any other type of professional advice of any kind or nature whatsoever. Audience members should refrain from taking action based on this material without first consulting with their own attorney, tax adviser, or financial adviser.